A rise in interest in stock investments and more home sales occurred simultaneously, resulting in an increase of over 9 trillion South Korean won in household loans during the previous month. Financial regulators have implemented actions such as lowering credit loan caps for those with higher incomes and reviewing banks' adherence to residential lending contracts.

On the 11th, the Financial Services Commission stated in its *‘May Household Loan Trends’* report that total household loans from all financial institutions rose by 9.3 trillion South Korean won during the previous month. This represents about 2.7 times the growth seen in April (3.5 trillion South Korean won) and far surpasses the rise of 5.9 trillion South Korean won observed in May of the prior year.

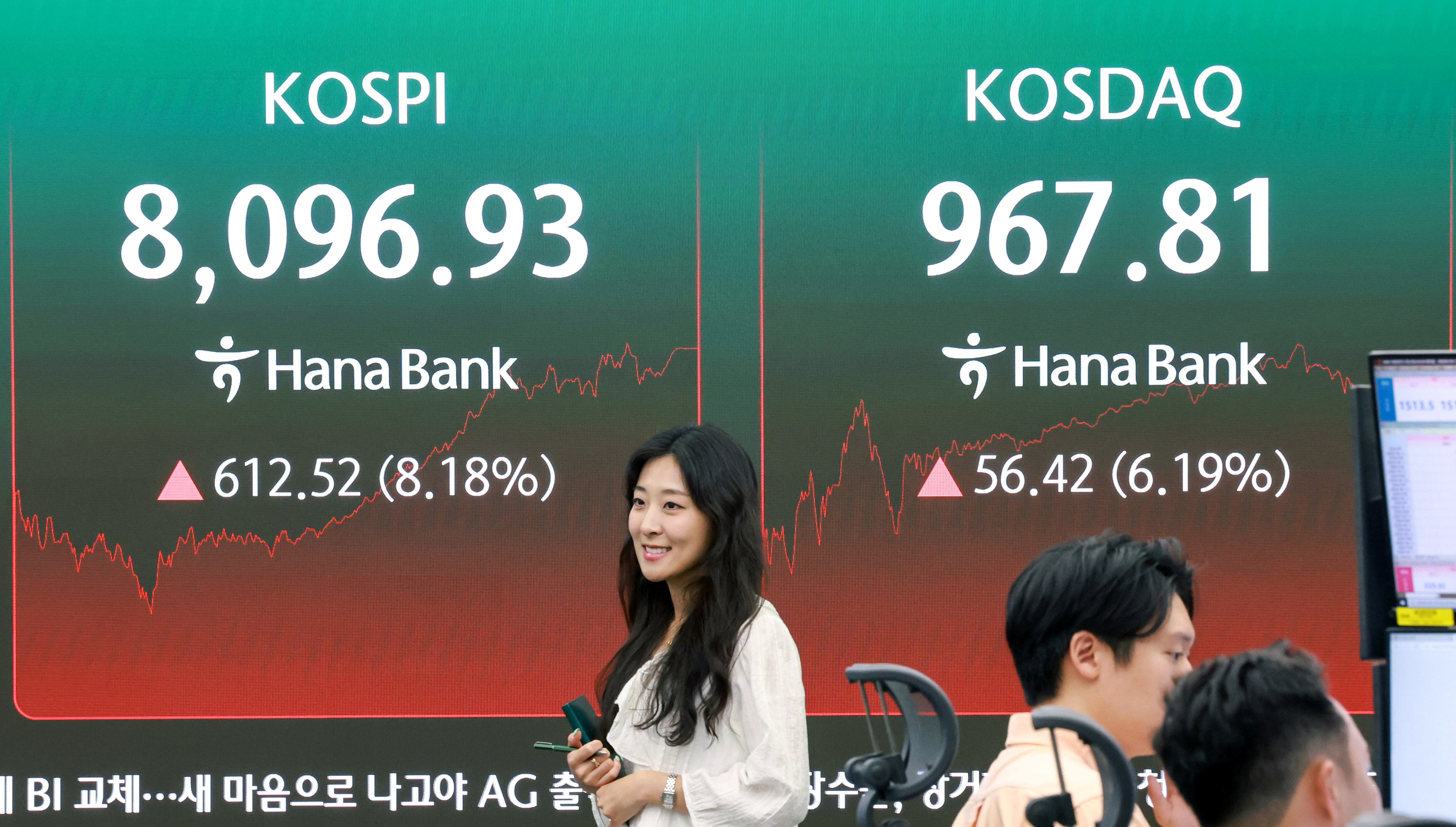

With a notable surge in the KOSPI lately, credit loans were responsible for the growth in borrowings. Other types of loans, such as credit loans, experienced a dramatic shift—from a decline of 2 trillion South Korean won in April to an increase of 5.3 trillion South Korean won in May. Particularly, loans under bank-sector negative accounts grew substantially, moving from a drop of 600 billion South Korean won in April to a gain of 2.6 trillion South Korean won in May. Increased consumer spending during Family Month also played a role.

Residential mortgage loans rose by 4 trillion South Korean won, continuing at a high level after an increase of 5.5 trillion South Korean won in the prior month. Nevertheless, due to higher apartment sales in the metropolitan area and broader implementation of approved bulk loan programs, the growth rate of residential mortgage loans saw a slight decline from the previous month. Shin Jin-chang, Director of the Office at the Financial Supervisory Service, said, "It is possible that residential mortgage loans could grow once more as property listings get absorbed following the end of the deferral period for the supplementary capital gain tax on multi-homeowners."

Authorities have introduced an emergency management framework, which involves holding weekly gatherings with financial organizations that haven't met goals related to managing consumer debt. Significantly, the banking industry intends to cut new loan caps for individuals with higher incomes and promote early repayment of credits by waiving charges associated with repaying loans before their scheduled term. The Financial Regulatory Agency will carry out ongoing audits to confirm that banks follow previous agreements they've reached with borrowers when issuing loans, such as promises to sell existing homes, restrictions on buying more properties, and relocation requirements.